Sometimes while experiencing life, influences align positively magnifying the in-ordinary to extraordinary. The opposite is also true. A few weeks ago, Cirrus Logic (CRUS) reported its full FY18 year and March quarter results. The headline numbers certainly didn't impress. Yet, often headline numbers deceive. Although short-term, the numbers offered no deception, the hidden reasons for the negative results were influenced significantly by inventory management from a major customer possibly because of coming products changes. The shareholder letter also included a statement many might consider a short-term death clause, "Based on our current visibility and the weaker than anticipated outlook for Q1 FY19, we now expect revenue for the full fiscal year to be down approximately 10 percent year over year." It is important to focus on the words, "current visibility."

Comparison of YoY and Financial ResultsFirst, let us review last year's financial performance. In the shareholder letter, the company wrote, "Revenue for the year was below our expectations due to lower than anticipated smartphone unit volumes." Revenue for FY18 was basically unchanged, flat YoY; earnings were down $0.25 YoY from $4.5 in FY17, due mainly to higher R&D costs. Headcount at Cirrus increased by 150 adding approximately $12 million in employee costs or a reduction of $0.20 in earnings. In calculating the reduction, our basis was $150,000 per employee for a full year. We used half of the full year total cost of $25 million. Margins for FY18 continued to creep up reaching 49.7 versus 49.2 the prior year.

One customer contributed 79 percent of sales (Apple (AAPL)) in the March quarter for FY18 virtually unchanged with the March FY17 quarter of 78%. March's revenue for FY18 was down $20 million YoY at $305 million.

Considering the December and March quarters (YoY), Cirrus' revenue dropped by $20 million for March and $40 million for December. This revenue drop seems strange in that Cirrus now ships an additional DAC product in a slightly higher percentage for Apple iPhones. Driven by iPhone product mix, Cirrus has been enjoying a slightly higher iPhone ASP since the middle of the September quarter. Given that Apple has sold virtually the same number of phones YoY since the September quarter, this $60 million drop in revenue seems disconcerting. We note that in our belief, Apple sold 73 million units in the December 2017 quarter not its headline of 77 million.

Finally, the company purchased 1.4 million shares at an average price of $42 dropping the fully diluted share count to 64.5 million while ending the quarter with approximately $450 million in cash. The market softness left inventories higher at the end of the March quarter ($205 million) than at the end of December ($193 million).

The -10% YoY Revenue GuidanceOn the surface, the lower revenue in FY18 and lower -10% FY19 guidance also seems troublesome. A possible loss of 10% in FY19 revenue over FY18 calculates to an additional drop of $150 million. A large portion of the $150 million comes in the June quarter being approximately $80 million ($240 million upper end of June 2018 guidance versus $320 million a year ago). Why the difference when analysts and Apple guidance suggest iPhones sales of 40-45 million units similar to June 2017 quarter? A first analysis of the numbers might suggest that Cirrus lost ASP. We found no evidence supporting this. In fact, while answering a question about Apple, Cirrus CEO, Jason Rhode, commented, "We don't see our opportunities there shrinking or going away in any way."

Analyzing Cirrus' June quarter last year provides insight into a large piece of the difference. The June revenue equaled $320 million of which $245 million was from Apple. Apple sold 9 million iPads equaling $17 million Cirrus revenue and 4 million Macs totally approximately $8 million. Apple sold 40 million iPhones at an approximate ASP of $4.9 or $195 million in revenue. The total products sold represents $215 million or $25 million less than Cirrus reported. It was and is our belief that Apple added some inventory during the June quarter 2017. We didn't see the same increase in inventory with Apple in this year's June guidance. In fact, we calculated the opposite. Our observations in the past suggest that when Apple makes major inventory changes with Cirrus during the June quarter, expect to see new versions of Cirrus parts coming in September. Rhode added depth to this thought, "But I mean, we've got a meaningful number of tape-outs this quarter that are all kind of [revet] zero all-in expensive, fine-line geometry processes, some of which are targeted at the next part in the product line to maintain share, and as usual, try to grow a little bit of content in the process."

To check our belief, we calculated by quarter approximate Cirrus part inventories for the last 5 quarters with the June quarter of last year being the beginning quarter. Changes in the value of Apple inventory shown in millions of dollars are listed in the following table. To calculate the results, we used ASPs for iPads and Mac Computers of $2 combined with a rounded number of unit sales from Apple reports. For the June 2018 quarter estimate, the calculation assumed 42 million iPhones sold, plus 4 million Macs, 9 million iPads, revenue of $240 million and 78% of its revenue from Apple, numbers similar to last June. With this approximate model, the beginning surplus of $25 million is the same as the ending surplus. If Apple truly sells 40-45 million iPhones in the June quarter, we expect the Cirrus' revenue to be between $240-250 million. In essence, Apple's inventory management created a huge difference of $80 million between this year's June guidance and last year's June guidance, pretty amazing.

| Quarter | June 17 | Sept. 17 | Dec. 17 | March 18 | June 18 (Estimate) | Sum |

| Part Value Differences in Millions | 25 | 84 | 16 | -49 | -49 | 25 |

We suspect also that the Galaxy S9 unit sales in which Cirrus provides parts might be extremely weak. In Korea, the new Galaxy volumes are at record lows. This might explain Cirrus conference comment, "Let's be mindful of slowing growth in some of the markets that we serve."

The rest of the 10% drop guided by Cirrus for the rest of the year seems to us any way to be from slightly lower iPhone ASPs with Apple no longer including the dongle with new iPhones. In recent articles, we have estimated this loss of revenue at $75 million. The total possible loss of revenue from Apple inventory management and lost dongle is $150 million or 10%. The perfect storm created from Apple inventory management, possible new part updates, weak Galaxy S9 phones, and a future temporary lower iPhone ASP seems to be creating the illusion of major structural issues for Cirrus' key businesses. We believe it is nothing more than a perfect storm of negative issues. The following comment again from the call supports our view. Rhode answered, "We don't see a turning point around optimizing around a small handful of not great quarters because there's nothing really meaningfully changed about the outlook we have for the longer term." We hope our findings help explain the validity of the company's stance.

FY19 Expected Earnings and CashCalculating earnings includes several factors, revenue, gross margin, operating costs, tax rates and share count. The first parameter revenue is the most difficult. Near of the end of the last conference call Jason added "And if things turn out to be more exciting, then that way, we can be positively priced." and "I think out takeaway from last year is just be conservative on modeling that sort of thing as it relates to external communication. And then if it's better than that, then we'll be positively surprised." The company views the 10% drop as worse case. In our view, a positive $25-50 million from Apple replenishing inventory with possible new parts begins our base case revenue calculation. We also believe that Cirrus has some new business coming later in the year. If iPhone sales remain flat, we believe that the base case revenue is minus $100 million or $1.4 billion for FY19.

Because gross margins have been increasing slowly, we are modeling this fiscal year at 50%. The companies guided operating costs for the following four quarters at the mid-point of the June quarter GAAP guidance of $133-139 million with $26 million in non-GAAP write offs. The operating costs for the year would be $110 million times 4 or $440 million. The company guided this year's tax rate at 17%. The base case earnings become $1.4 billion times 0.5 - $0.44 billion times .83 or $215 million. The almost $500 million in cash could generate an additional $10 million in interest bringing the total base case to $225 million.

Cirrus purchased 1.4 million shares last quarter with $200 million (5 million shares at $40) still available. We believe that the average share count for the coming year will be 2.5 million lower than the most recent count or 62 million. It could be lower. Our base earnings are $225 million divided by 62 or $3.6.

Ranging Next Year's EarningsSeveral positive factors seem to make $3.6 too low. First, in the past several quarters, Cirrus operated near the middle yet lower portion of its guidance. With costs in its crosshairs, we believe that operating costs will actually average near the low end of the June guidance or at $107 million a quarter. With $12 million lower costs, earnings could be $0.15 higher.

The biggest factor is iPhone unit sales. This past year's super cycle turned into a super super super duper duper DUD. We discussed this issue in other seeking alpha articles. In our view, Apple is better managing its coming iPhone product cycle with the alleged three new phones coming in September. Apple could sell an increased number of phones with a product cycle more in tune with its ecosystem. Each 10 million phones sold adds about $0.35 in earnings. With a base case at $3.6, FY19 earnings will likely range from $3.75 to $4.25. Unless Apple throws another DUD cycle, we expect earnings at the upper end of the range.

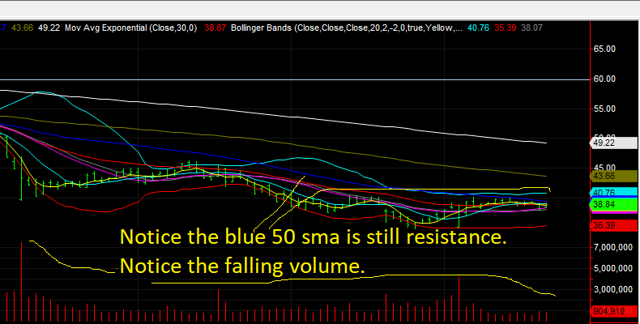

Technical ChartsThe two following self-created charts on Cirrus point out the significance of the $40 price resistance point and the 50 simple moving average. The first chart uses 30-minute bars; the second consists of day bars.

The company included some interesting statements regarding future products and direction.

"We expanded our product portfolio to span a more diverse range of solutions for flagship and mid-tier devices and continued to increase our penetration of the Android market with new and existing customers. The company also introduced innovative new technologies that we believe will drive meaningful growth opportunities in both existing and new adjacent markets, including our 28-nanometer voice biometrics component and 55-nanometer audio and haptic boosted amplifiers." With respect to haptics, "We are pleased to have secured our lead design win with first-generation haptic products which is expected to begin shipping later this year and we are engaging with customers on our second-generation component." By the way, the second-generation product includes an always on (AWO) feature.

Cirrus also added that the largest OEMs are designing both wired and wireless active noise cancelation headsets. This by itself could be a huge revenue generator.

The shareholder also contained this bit of information, "As we look further out, we recognize that our business model requires a substantial investment in future R&D efforts, and we are actively engaged in adjacent domains that we believe will provide new opportunities beyond audio and voice as we leverage our mixed-signal and low power signal processing expertise." Haptics development is one of the new businesses. We also saw an interesting job opening a few months ago for a position to work in a new instrumentation/sensor group with the first products being new advanced microphones.

We found this statement made during the conference call extremely interesting, "And while it's always nice to have a really great strategy, it's also really nice to have your primary competition, particularly in China and the rest of the Android space, it's always nice to have your competition have a bunch of, I would say, challenges pop up at the same time."

What Are We Doing?Several indicators including short interest, resistance points, mutual fund purchases and company buying taken together give a mixed signal (pun intended). The short interest is still high almost 10 million shares up from its low several quarters ago of 3 million. The chart confirms a very significant resistance point at 40. Our included charts also confirm a reasonable bottoming of the stock near $35.

But, for us, two important factors turned positive, the mutual fund company, FMR, began purchasing last quarter adding 1.25 million shares. FMR has long been an extremely successful trader of Cirrus. Several years ago, with Cirrus trading near $10, FMR purchased selling out in the high $30's to low $40's. FMR, again some years ago, purchased Royce's near 7 million shares under $20 and recently sold most of its shares above $60. The mutual fund is once again buying. Last quarter, the company purchased 1.4 million shares commenting that it planned to continue doing so. We are buying slowly at prices under $40. We also are trading out recent purchases near $40 if we began to suspect continued resistance under $40. We are following the company and FMR. Sometimes perfect storms happen. When understood, they create buying opportunities. Still enduring them isn't fun.

Disclosure: I am/we are long CRUS.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: We are long Cirrus and adding shares from time to time. We are also selling the recent share additions as we continue to sense resistance.

No comments:

Post a Comment