Image: Semisub Transocean Leader

Investment Thesis

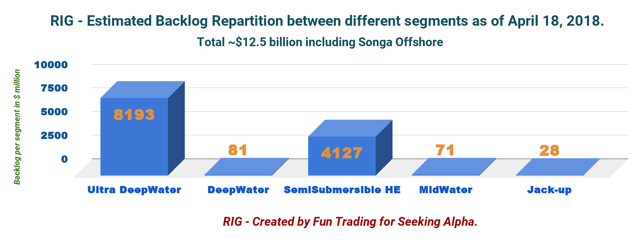

Transocean (NYSE:RIG) is one of the best offshore drillers with a record backlog of about ~$12.4 billion as of 05/2/2018 - not including options that could add over $8 billion - after the acquisition of Songa Offshore.

RIG is my most significant long-term investment in the offshore drilling sector, and I recommend accumulating the stock for the long term and, above all, ignoring what I call the "market noise" that tends to darken or brighten the picture unnecessarily.

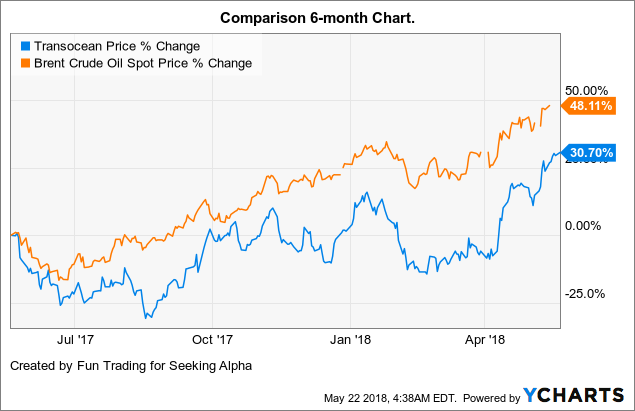

The stock has done quite well recently, after tumbling in February to $9+ despite the company again beating analysts' estimates in the fourth quarter. The stock is back to $13.75, after reaching a low at below $7.50 in August 2017.

However, looking at the 1-year chart above, we conclude that it is essential to trade a good part of your holding to take advantage of the volatility attached to the offshore drilling sector. About 30% seems right, at least for me.

Just a thought or two

Even though you may think otherwise, the offshore drilling industry is not doing exceptionally fantastic, though oil prices have been ultra-bullish recently due to a renewed geopolitical instability that favors a bullish oil price environment that I see as temporary. How "temporary" and how "high" is the question.

What is clear is that RIG moves in tandem with oil prices, and the strong momentum will keep pushing the stock higher only if oil continues to go higher. Or so it seems.

RIG data by YCharts

RIG data by YCharts

On the other hand, offshore drillers are visibly grappling to survive, while waiting for a potential recovery that appears elusive because oil operators are slow to contract again, and the industry suffers a persistent rig oversupply keeping dayrates at rock-bottom.

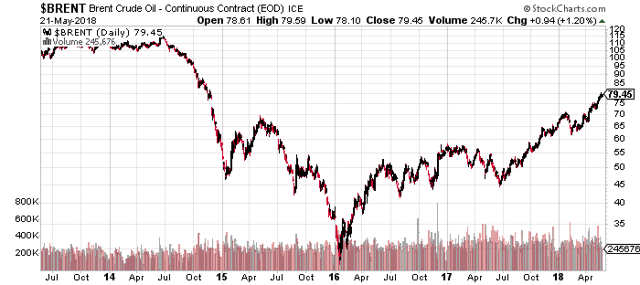

Nonetheless, oil prices are beginning to show significant momentum lately and are solidly trading above $70 per barrel, and now flirting with $80 a barrel - a rate not touched since November 2014.

Consequently, rig contracting activity and utilization should be on the rise; asset values should increase, and optimism is starting to get some serious momentum. Yes, "optimism" is one ingredient that the market never lacks at the beginning.

Still, contracting is not stellar, and beside some pockets of strength like the North Sea segment for the harsh-environment jack-ups and HE semisubmersibles and the Middle East, the floaters segment is still hibernating.

However, Jeremy Thigpen, CEO, had some encouraging comments in the most recent conference call about the deepwater market:

With this supply dynamic playing out, combined with current offshore breakeven economics for most projects at levels ranging from the 40s to as low as the low 20s, it's not surprising to see increasing customer interest in the offshore developments. In fact, if oil prices can remain constructive for the next few months, we believe that operator budgets for 2019 could reflect a return to offshore projects sanctioning for 2019 and beyond as the deepwater space has become a more compelling investment proposition for our customers.

Noble Corp. (NYSE:NE), which released its first-quarter 2018 results recently, is another example. Robert W. Eifler, Noble's Vice President and General Manager - Marketing and Contracts, said on the company's latest conference call:

While fixture activity in the deepwater space has developed more slowly this year than we had hoped, global liquids demand has remained strong; breakeven costs offshore are now largely below $50 per barrel; projects sanctions doubled 2017 over 2016; and we believe that we remain on the cusp of notable improvement in the segment.

Unfortunately, the deepwater recovery is still on hold after six months of calling it "knocking at the door." Hopefully, it will materialize in H2 2018, at least that is what Ocean Rig UDW (NASDAQ:ORIG) is suggesting.

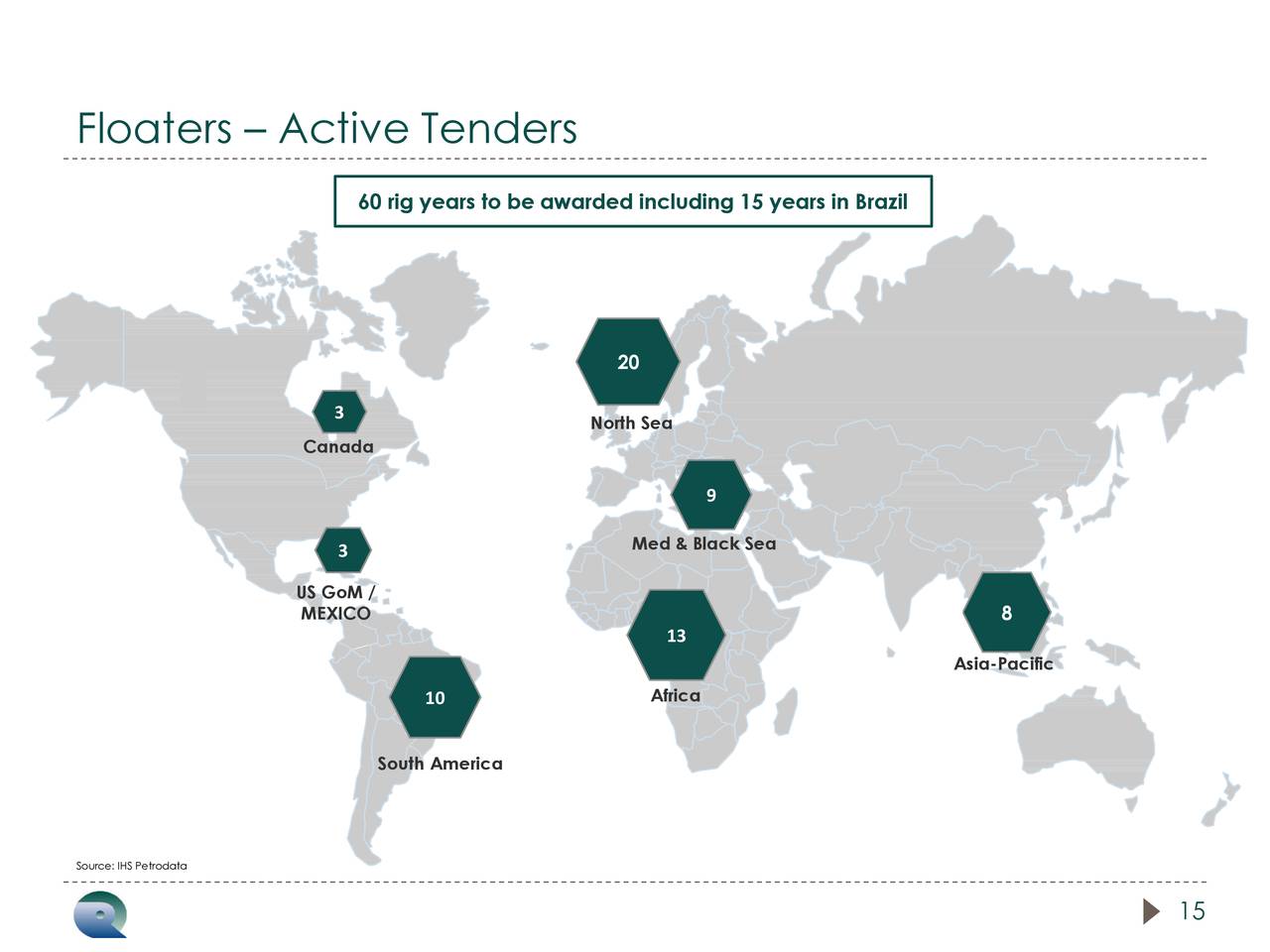

One important element that Mr. Pankaj Khanna, ORIG CEO, developed was that a lot of floaters active tenders are actually going on, representing 60 rig years to be awarded soon, with the lion's share in the North Sea.

Source: Last ORIG Presentation

One example of this surge in activity in the North Sea particularly is the recent contract awarded by Azinor Catalyst to the semisub Transocean Leader:

Azinor Catalyst said on Tuesday that the Transocean Leader, a semi-submersible, will be provided to drill a well to appraise the company��s Agar �� Plantain opportunity. The company is currently in the advanced stages of planning and preparation for the well which, subject to the receipt of required regulatory approvals, is scheduled to spud in 3Q 2018.

One caveat that tells me a lot about this rally

It is now clear that the deepwater and ultra-deepwater have not shown any definitive signs of a nascent recovery, despite the fact that we are experiencing a bullish momentum in oil prices, which are now trading at nearly $80 per barrel and look like a magic bullet for the offshore industry somehow. I think I have demonstrated this idea above.

We should be optimistic, though! But realistic.

Signs abound to justify a recovery later this year, or so it seems. The actual number of tenders around the world for floaters is impressive, but are they telling the true story? Not totally, in my opinion, and here is why.

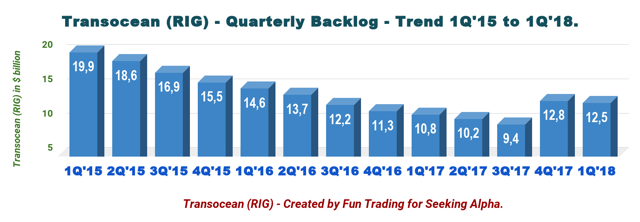

The offshore drilling industry needs a strong backlog that reverses the long trend of destruction that offshore drillers experienced since 2014, as the Transocean quarterly backlog trend chart illustrates below.

(Note: Do not pay attention to the last two quarters, because RIG acquired Songa Offshore and over $3 billion of backlog. Without this acquisition, the backlog would be below $9 billion by now.)

One caveat that should never be set aside in assessing the health of the Industry is explained by Pankaj Khanna, who said in the last ORIG conference call:

However, the length of programs awarded is quite short as reflected by the graph on the left. This reflects the phenomenon of the last couple of years, where most of the development projects have been field expansions, Phase 2s and tie-backs and very little exploration. Therefore, most oil companies have been taking rigs for a well-by-well campaign

About the nature of the floaters recovery

The deepwater and the ultra-deepwater are expected to recover later this year. However, this positive statement may not be sufficient to create the turnaround that the offshore industry desperately needs. At least for two reasons, essentially:

The length of the future program awarded is too short to fuel real optimism and reverse the backlog erosion experienced since 2014.

Oil operators are not investing enough exploration CapEx right now. Hopefully, this trend will change and could be considered the second phase of the recovery in H2 2019. However, we should expect a slow "U" recovery, not a "V" recovery.

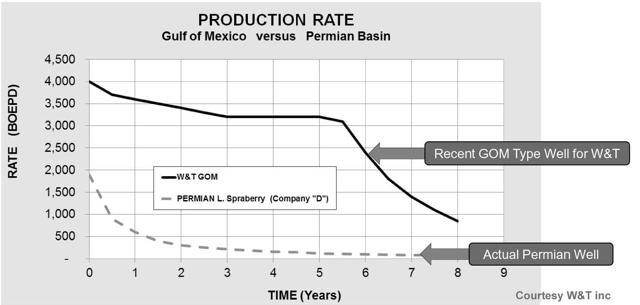

One explanation for this slow "reaction" from the oil operators is probably due to US shale. A large sustaining CapEx is necessitated to maintain and grow production in the shale due to the rapid depletion experience by a shale well, as illustrated by W&T Inc. (NYSE:WTI) in its last presentation and quarterly results that I covered recently.

The rig oversupply is concerning worldwide, besides the North Sea segment. The result is that the dayrate will not climb for a long period of many months or years after the recovery begins. This is true for floaters and jack-ups as well. Bassoe explained that the new economics weigh heavily on the overall attrition strategy, as I have explained in this article that I recommend you to read. However, while it is more oriented to the jack-ups segment, it gives some important insights on the general situation. Conclusion

Investors will have to be patient. The recovery is on its way, but will be at an "escargot" pace, in my opinion, and the benefits expected to the balance sheet will not be extraordinary despite the sheer exuberance of the actual market. Let's keep in mind, the offshore drilling industry is a service and will not profit directly from oil prices as oil producers do.

However, investing in an offshore drilling company such as RIG is an excellent long-term strategy, especially if you take some profit on the way when the market is overoptimistic and accumulate again when the market is overly pessimistic. A simple look at the 3-year chart is self-explanatory.

Author's note: Do not forget to "Follow" me on the oil sector. Thank you for your support, I appreciate it. If you find value in this article and would like to encourage such continued efforts, please click the "Like" button below as a vote of support. Thanks!

Disclosure: I am/we are long RIG.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Source: Shutterstock

Source: Shutterstock